User Center

User Center My Training Class

My Training Class Feedback

Feedback

Dry Bulk Newbuilding Orders Go “Extinct”, as Interest Limited to Tankers

In its latest weekly report, shipbroker Allied Shipbroking said that “key investment’ sentiment seems to have been split across the two key segments. On the one hand, the poor performance of the dry bulk freight market and the discouraging market outlook, at least for the time being, has trimmed any interest for new projects. It is important to state here that most of the new orders coming to light seem to be older transactions that have only just emerged. We expect activity to remain weak in the near-term, while any fresh interest that we may witness is expected to be focused mainly in the Panamax and Supramax segments. At the same time, the outlook for the tanker markets is at the moment much more bullish, something that is depicted in the intensifying interest noted amongst potential buyers for new orders amid a difficult period for the global economy. The main bulk of focus is expected to remain on the more versatile units such as Aframaxes and product tankers. Meanwhile, prices will play an important role over the coming period as it will shape how much of this interest will materialize over to actual transactions”.

In a separate weekly note, Banchero Costa said that “in the tanker market it was reported that C.M. Lemos ordered at Hyundai Samho 2 + 2 optional Suezmax tankers 158,000 dwt at a price of $61.45 mln each, with deliveries fixed for 2H of 2021-1st half of February 2022. Another Greek family Lykiardopulo (Neda Maritime) moved for 1 + 1 optional LR2 tankers 115,000 dwt at Daehan shipyard with delivery during 2021: price to be around $50 mln (no scrubber initially installed). In the dry market, it was recorded Japanese interest to move for Chinese shipyard. Dalian COSCO KHI (where Kawasaki H.I. is partner) received orders from Mitsui & co. and Dowa Line for 4 x Ultramax units (2 each) with deliveries for 2nd Half 2021 – 1st half 2023. Same yard received an order from Far East Shipping for one Ultramax with delivery June 2021. Total of 5 vessels will be build according to Kawasaki 61 design. Always in China, Mitsui & Co moved for 2 x Kamsarmax units at Jiangsu New Yangzijiang for a price around $26 mln each.

Meanwhile, in the S&P market this past week, Allied noted that “on the dry bulk side, a modest level of activity was seen for yet another week. The recent severe drop in freight rates though is expected to hurt market sentiment further and lead to decreased appetite from the side of buyers. However, last week we noted several new deals being reported, with focus given once again to the smaller size segments such as Supramaxes and Handysizes. This trend is not expected to change anytime soon, as buyers are looking for the security provided by the lower risk/lower volatile market segments. On the tankers side, things may be much more positive with regards to the current market outlook, but this has yet to be properly reflected in the volume being noted in the second hand market. Last week was no exception to this with a still slow flow of new deals coming to light. The bullish appetite is still dominating the segment though and thus it is likely that we will see further activity emerge over the coming weeks”.

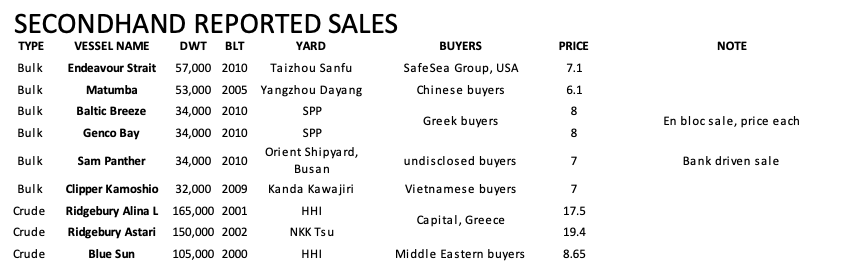

Banchero Costa added that “in the S & P market, the major concern was still the logistic in arranging inspection (although the leading independent companies performed excellent services) and taking delivery of ships couple with the expectations of further softening prices in the dry bulk segment. During the week the activity was focused predominantly on Handysize bulkers: 2 sisters x 35,000 dwt built in 2015 at Tsuneishi Cebu SWIFTNESS & SHARPNESS (fitted with BWTS) were sold to undisclosed interests (Greek based) for region $13 mln each. Stock listed Genco disposed 2 sisters Handysize x 35,000 dwt built in 2010 at SPP GENCO BAY & BALTIC BREEZE (both with SS due in 2020) for region $8 mln each to undisclosed buyer. Another similar Handysize bulk carrier SAM PANTHER 34,000 dwt built in 2010 at Orient shipyard (Korea) was reported sold for region $7 mln basis SS due end of 2020; the sale seemed to be driven and pushed by controlling bank. Following the recent trend of dolphin 57 being sold, another unit was sold: the AMAZONIT 57,000 dwt built in 2011 at Hantong with Tier II engine for a price of region $7.2 mln. In the same segment, the Crown 53 design MATUMBA 53,000 dwt built in 2006 was sold to undisclosed buyers (reported Chinese) for price of region $6.1 mln basis SS and BWTS due fairly prompt. In the tanker segment an interesting sale to report: a large VLCC resale of 300,000 dwt was sold by Sinokor to clients of Thenamaris for region $94 mln usd (scrubber fitted). In a different transaction the Handysize tanker CIELO DI GUANGZHOU 39,000 dwt built in 2006 by GSI was reported sold to undisclosed for $8.8 mln”, the shipbroker concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Comments

Something to say?

Log in or Sign up for free